| Media Relations: | Investor Relations: |

|---|---|

| Ashleigh Koss | Felix Lauscher |

| 908-981-8745 | +33 (0)1 53 77 45 45 |

| Email: [email protected] | Email: [email protected] |

Media Panel

Resources

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

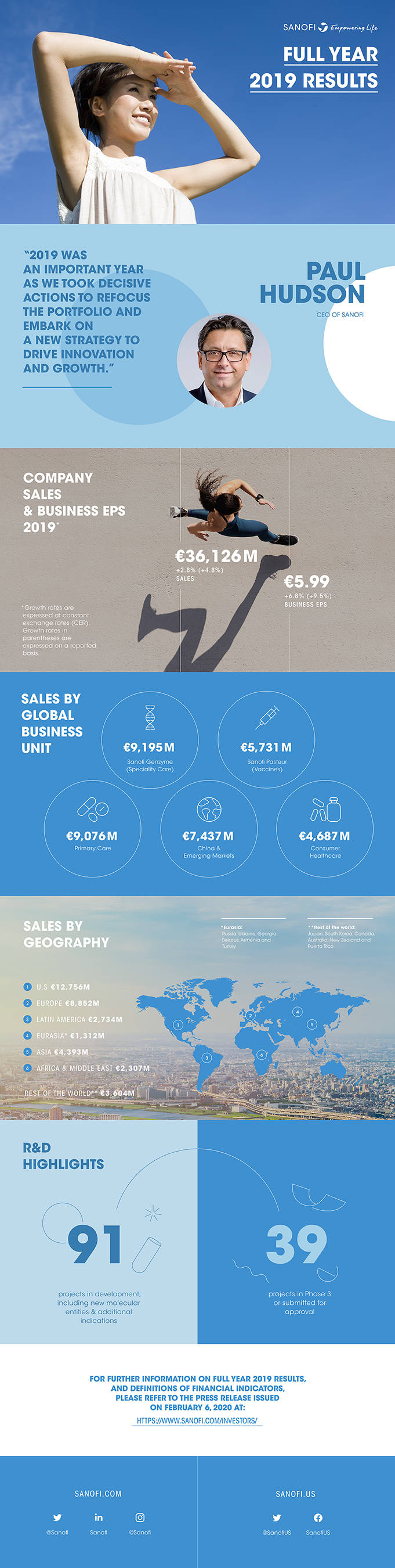

Sanofi delivers strong 2019 business EPS growth of 6.8% at CER

| Q4 2019 | Change | Change at CER | 2019 | Change | Change at CER | |

| IFRS net sales reported | €9,608m | +6.8% | +4.7% | €36,126m | +4.8% | +2.8% |

| IFRS net income reported | -€10m | -103.9%(2) | - | €2,806m | -34.8%(2) | - |

| IFRS EPS reported | -€0.01 | -105.0%(2) | - | €2.24 | -35.1%(2) | - |

| Business net income(1) | €1,684m | +23.5% | +18.4% | €7,489m | +9.8% | +7.0% |

| Business EPS(1) | €1.34 | +21.8% | +17.3% | €5.99 | +9.5% | +6.8% |

Fourth-quarter 2019 sales performance(3) driven by Dupixent® and Vaccines

- Net sales were €9,608 million, up 6.8% on a reported basis and 4.7%(3) at CER.

- Dupixent® (global sales €679 million, up 135%) the largest growth contributor, drove Sanofi Genzyme GBU sales up 19.7%.

- Vaccines sales increased 22.0%, reflecting majority of U.S. influenza vaccine shipments in Q4.

- CHC sales down 5.2%, mainly due to Zantac® voluntary recall, non-core divestments and changing regulatory requirements.

- Primary Care GBU sales declined 8.7% due to lower sales in Diabetes and Established Products.

- Lower China sales (down 21.0%) due to anticipated price and inventory adjustments on Plavix® and Avapro® in the channel.

Full-year 2019 sales growth of 3.6% at CER/CS(4) and business EPS growth of 6.8% at CER

- Net sales were €36,126 million, up 4.8% on a reported basis and 2.8% at CER (up 3.6% at CER/CS(4)).

- Dupixent® sales reached €2,074 million, on track with ambition to achieve more than €10 billion peak sales.

- Vaccines sales increased 9.3% to €5,731 million, supporting expected mid-to-high single digit CAGR from 2018 to 2025.

- Business operating income margin improved 1.2 percentage points to 27.0%, trending towards objective of 30% by 2022.

- Q4 2019 business EPS(1) up 17.3% at CER to €1.34.

- Full-year 2019 business EPS of €5.99 up 6.8% at CER.

- Full-year 2019 IFRS EPS of €2.24 (down 35.1%(2)), reflecting a €3.6 billion impairment charge mainly related to Eloctate®.

- Board proposes annual dividend of €3.15, the 26th consecutive increase in dividend.

Significant R&D advances and regulatory milestones

- SAR442168, a BTK inhibitor, achieved proof of concept in relapsing multiple sclerosis; phase 3 program to be initiated mid-2020.

- Dupixent® submitted to FDA (priority review) and EMA as first biologic for children aged 6-11 years with atopic dermatitis.

- Dupixent® phase 3 pivotal studies initiated in bullous pemphigoid, chronic spontaneous urticaria and prurigo nodularis.

- Dupixent® efficacy and safety further supported by 3-year data from OLE (Open Label Extension) study.

- Fluzone® High-Dose Quadrivalent approved in the U.S.

- Sutimlimab demonstrated positive phase 3 results in cold agglutinin disease.

- SAR408701, an anti-CEACAM5 antibody-drug conjugate, entered into phase 3 in non-small cell lung cancer.

- Olipudase demonstrated positive pivotal topline data in adult and pediatric patients with acid sphingomyelinase deficiency.

- Successful completion of Synthorx acquisition enhances Sanofi’s position as an emerging leader in oncology and immunology.

2020 financial outlook

Sanofi expects 2020 business EPS(1) to grow around 5%(5) at CER, barring unforeseen major adverse events. Applying average January 2020 exchange rates, the positive currency impact on 2020 business EPS is estimated to be around 1%.

Sanofi Chief Executive Officer, Paul Hudson, commented:

“I am encouraged by the fourth quarter results which position Sanofi to deliver on our new strategic priorities. The acceleration in sales performance was mainly driven by the impressive growth of Dupixent®, our transformative medicine for type 2 inflammatory diseases and by our differentiated Vaccines portfolio. At the same time, our sharpened focus on operating and financial efficiencies helped us to deliver margin expansion and significant cash flow improvement. We are making great progress in our ambition to transform Sanofi R&D and I am particularly excited by the positive proof of concept data for our BTK inhibitor, a potentially practice changing therapy for multiple sclerosis, announced today. There is increasing momentum across the entire Sanofi organization and I am confident we will achieve the long-term growth aspirations and margin targets we set out at our Capital Markets Day”.

(1) In order to facilitate an understanding of operational performance, Sanofi comments on the business net income statement. Business net income is a non-GAAP financial measure (see Appendix 11 for definitions). The consolidated income statement for Q4 2019 is provided in Appendix 3 and a reconciliation of reported IFRS net income to business net income is set forth in Appendix 4; (2) Q4 2019 and full-year 2019 included impairment charge of €1,581 million and €3,604 million, respectively, mainly related to Eloctate®; (3) Changes in net sales are expressed at constant exchange rates (CER) unless otherwise indicated (see Appendix 11); (4) Constant Structure: Adjusted for divestment of European generics business and sales of Bioverativ products to SOBI; (5) Base for business EPS growth is €5.97, reflecting 2 cents impact from IFRS 16 (see appendix 11).

R&D update

Consult Appendix 9 for full overview of Sanofi’s R&D pipeline

Regulatory update

Regulatory updates since October 31, 2019 include the following:

- In November, Dupixent® (collaboration with Regeneron) was submitted to the FDA in children 6 to 11 years with moderate-to-severe atopic dermatitis.The FDA has granted a priority review and set a PDUFA date of May 26, 2020. Dupixent® was also submitted for the same indication in the European Union in January.

- In November, the FDA approved a supplemental NDA expanding the indication for Toujeo® in the United States to include the treatment of pediatric patients 6 years and older with diabetes.

- In November, the FDA approved a supplemental Biologics License Application for Fluzone® High-Dose Quadrivalent (influenza vaccine) for use in adults 65 years of age and older.

- In December, the China National Medical Products Administration (NMPA) approved Praluent® for the treatment of adult patients with primary hypercholesterolaemia or mixed dyslipidemia and for the treatment of adult patients with established atherosclerotic cardiovascular disease to reduce myocardial infarction, stroke or unstable angina requiring hospitalization.

- In December, the China National Medical Products Administration (NMPA) approved Fabrazyme® as a long term enzyme replacement therapy in patients with confirmed diagnosis of Fabry disease.

- In January, the European Commission approved the expansion of the indication for Toujeo® in the European Union to include the treatment of diabetes in adolescents and children (6 years and older).

At the beginning of February 2020, the R&D pipeline contained 91 projects, including 38 new molecular entities in clinical development (or that have been submitted to the regulatory authorities). 39 projects are in phase 3 or have been submitted to the regulatory authorities for approval.

Portfolio update

Phase 3:

- Three-year data from the OLE (Open Label Extension) study of Dupixent® supporting the long term efficacy and safety profile were presented at the Maui Dermatology Conference in January.

- Positive results of a pivotal phase 3 open-label, single-arm trial evaluating the safety and efficacy of sutimlimab in people with primary cold agglutinin disease (CAD) were presented at the Late Breaking Abstracts Session of the Annual Meeting of the American Society of Hematology. This study met its primary and secondary endpoints.

- Positive results from the EDITION JUNIOR phase 3 trial, evaluating Toujeo® in children and adolescents with type 1 diabetes, were presented at the International Society for Pediatric and Adolescent Diabetes Annual Conference.

- SAR408701, an anti-CEACAM5 antibody-drug conjugate, entered into phase 3 in second and third line non-small cell lung cancer (NSCLC).

- Dupixent® entered into phase 3 in bullous pemphigoid, chronic spontaneous urticaria and prurigo nodularis.

- BIVV001 (recombinant coagulation factor VIII Fc) entered into phase 3 in hemophilia A.

Phase 2

- BTK inhibitor, SAR442168, met the primary endpoint in a proof of concept trial in relapsing multiple sclerosis, with detailed results expected to be presented at an upcoming medical meeting in Q2 2020.

- Olipudase alfa, a recombinant human acid sphingomyelinase, demonstrated positive results in two separate clinical trials evaluating olipudase alfa for the treatment of acid sphingomyelinase deficiency (ASMD) in adult and pediatric patients. Olipudase alfa is the first and only investigational enzyme replacement therapy in late-stage development for the treatment of ASMD. No treatments are currently approved for ASMD.

- SAR439859, a selective estrogen receptor degrader (SERD), has entered into a pivotal phase 2 study in second and third line metastatic breast cancer as a monotherapy, a phase 2 study to enable examination in the adjuvant setting, and a phase 1 combination with palbociclib.

Phase 1

- A candidate vaccine for Yellow Fever entered into phase 1.

- THOR-707, an engineered “not-alpha” IL-2, entered into phase 1 for the treatment of solid tumors, with the acquisition of Synthorx.

- SAR441000, an mRNA-based intratumoral immunotherapy, entered into phase1 in combination with PD-1.

Synthorx

- On January 23, Sanofi announced the completion of its acquisition of Synthorx, enhancing Sanofi’s position as an emerging leader in the area of oncology and immunology. Through the acquisition Sanofi gained access to THOR-707 and an innovative platform that complements the company’s oncology and immunology research.

Sustainable performance update

Sanofi’s leadership in water management was recently recognized by CDP in its rating upgrade to A- from B. CDP is a global non-profit organization that drives companies and governments to reduce greenhouse gas emissions, safeguard water resources.

Sanofi considers water as a sustainable renewable resource and believes that shortages of water could become a major obstacle to public health involving diseases associated with lack of access to safe drinking water, inadequate sanitation and poor hygiene. Consequently the company has implemented a dedicated program to reduce water consumption and promote its reuse. Sanofi has already exceeded its 2020 target to reduce water consumption.

2019 fourth-quarter and full-year 2019 financial results(9)

Business Net Income(9)

In the fourth quarter of 2019, Sanofi generated net sales of €9,608 million, an increase of 6.8% (up 4.7% at CER). Full-year 2019 sales were €36,126 million, up 4.8% on a reported basis (up 2.8% at CER).

Fourth-quarter other revenues increased 24.3% (up 20.4% at CER) to €409 million, reflecting the VaxServe sales contribution of non-Sanofi products (€358 million, up 32.4% at CER). Full-year 2019 other revenues increased 24.0% (up 18.0% at CER) to €1,505 million, driven by the VaxServe sales contribution of non-Sanofi products (€1,273 million, up 26.3% at CER) and the consolidation of collaboration revenues from Swedish Orphan Biovitrum AB (SOBI).

Fourth-quarter Gross Profit increased 6.0% to €6,562 million (up 3.8% at CER). The gross margin ratio decreased 0.5 percentage points to 68.3% (68.2% at CER) versus the fourth quarter of 2018. The negative impact from net price adjustments of inventory in the channel in China, products and geographical mix in CHC, U.S. Diabetes net price evolution and Vaccines more than offset the favorable impact from Dupixent® growth. In the fourth quarter of 2019, the gross margin ratio of segments were 72.8% for Pharmaceuticals (up 0.7 percentage points), 64.5% for CHC (down 1.5 percentage points) and 60.1% for Vaccines (down 0.3 percentage points). Full-year 2019 Gross Profit increased 5.3% to €25,657 million (up 3.1% at CER). In 2019, the gross margin ratio increased 0.3 percentage points to 71.0% (70.8% at CER) versus 2018.

Research and Development (R&D) expenses increased 0.5% to €1,687 million in the fourth quarter of 2019. At CER, R&D expenses decreased 0.7% reflecting smart spending initiatives as well as portfolio prioritization. In the fourth quarter, the ratio of R&D to sales decreased 1.1 percentage points to 17.6% compared to the fourth quarter of 2018. In 2019, R&D expenses increased 2.2% to €6,022 million (up 0.2% at CER). In 2019, the ratio of R&D to sales was 0.4 percentage points lower at 16.7% compared to 2018.

Fourth-quarter selling general and administrative expenses (SG&A) increased 0.1% to €2,724 million. At CER, SG&A expenses were down 1.4%, reflecting a decrease in general expenses which more than offset increased investments in Specialty Care and Vaccines. In the fourth quarter, the ratio of SG&A to sales decreased 1.8 percentage points to 28.4% compared to the fourth quarter of 2018. In 2019, SG&A expenses increased 0.5% to €9,880 million (down 1.4% at CER). In 2019, the ratio of SG&A to sales was 1.2 percentage points lower at 27.3% compared to 2018.

Fourth-quarter operating expenses were €4,411 million, an increase of 0.3% and a decrease of 1.2% at CER. Full-year 2019 operating expenses were €15,902 million, an increase of 1.1% and down 0.8% at CER.

Fourth-quarter other current operating income net of expenses was -€70 million versus -€148 million in the fourth quarter of 2018. In the fourth quarter of 2019, this line included an expense of €241 million (versus an expense of €65 million in the fourth quarter of 2018) corresponding to the share of profit to Regeneron of the monoclonal antibodies Alliance, reimbursement of development costs by Regeneron and the reimbursement of commercialization-related expenses incurred by Regeneron. In the fourth quarter of 2019, this line also included a one-time income due to a legislation change related to supplementary pension plans in France. In the fourth quarter of 2018, the “other current operating income net of expenses” line also included charges related to a legal contingency provision as well as a capital gain on an associate company and other accruals, which in aggregate represented a net charge of €72 million. In 2019, other current operating income net of expenses was -€382 million versus -€64 million in 2018. The full-year 2019 expense associated with the monoclonal antibodies Alliance with Regeneron was €681 million, which compared with an expense of €211 million in 2018 (see appendix 7 for further details).

The share of profit from associates was €119 million in the fourth quarter versus €121 million in 2018, mainly reflecting the share of profit in Regeneron. In 2019, the share of profit from associates was broadly stable at €420 million versus €423 million in 2018.

In the fourth quarter, non-controlling interests were -€8 million versus -€22 million in prior period, reflecting the end of non-controlling interests related to the Alliance with Bristol-Myers Squibb on Plavix® and Avapro®. In 2019, non-controlling interests were -€35 million versus -€106 million for 2018.

(9) See Appendix 3 for 2019 fourth-quarter consolidated income statement; see Appendix 11 for definitions of financial indicators, and Appendix 4 for reconciliation of IFRS net income reported to business net income.

Fourth-quarter business operating income increased 26.0% to €2,192 million. At CER, business operating income increased 20.9%. The ratio of business operating income to net sales increased 3.5 percentage points to 22.8% versus the fourth quarter of 2018. Over the period, the business operating income ratio of segments were 28.7% for Pharmaceuticals (up 1.6 percentage points), 27.3% for CHC (down 1.7 percentage points) and 37.6% for Vaccines (up 1.5 percentage points). In 2019, business operating income was €9,758 million, up 9.8% (up 7.1% at CER). In 2019, the ratio of business operating income to net sales increased 1.2 percentage points to 27.0%.

Net financial expenses were -€63 million in the fourth quarter versus -€60 million in the same period of 2018, reflecting lower cost of net debt. The fourth quarter of 2018 included a gain of €22 million in the market value of a financial investment. Full-year 2019 net financial expenses were -€264 million versus -€271 million in 2018.

Fourth-quarter and full-year 2019 effective tax rate were 22.1% and 22.0%, respectively. Sanofi expects its effective tax rate to be around 22% in 2020.

Fourth-quarter business net income(9) increased 23.5% to €1,684 million and increased 18.4% at CER. The ratio of business net income to net sales increased 2.3 percentage points to 17.5% versus the fourth quarter of 2018. In 2019, business net income(9) increased 9.8% to €7,489 million and increased 7.0% at CER. The ratio of business net income to net sales increased 0.9 percentage points to 20.7% versus 2018.

In the fourth quarter of 2019, business earnings per share(9) (EPS) increased 21.8% to €1.34 on a reported basis and 17.3% at CER. The average number of shares outstanding was 1,253.1 million versus 1,245.6 million in the fourth quarter of 2018.

In 2019, business earnings per share(9) was €5.99, up 9.5% on a reported basis and up 6.8% at CER. The average number of shares outstanding was 1,249.9 million in 2019 versus 1,247.1 million in 2018.

Reconciliation of IFRS net income reported to business net income (see Appendix 4)

In 2019, the IFRS net income was €2,806 million. The main items excluded from the business net income were:

- An amortization charge of €2,146 million related to fair value remeasurement on intangible assets of acquired companies (primarily Genzyme: €727 million, Bioverativ: €488 million, Boehringer Ingelheim CHC business: €240 million, Aventis: €197 million) and to acquired intangible assets (licenses/products: €102 million). An amortization charge of €510 million related to fair value remeasurement on intangible assets of acquired companies (primarily Genzyme: €177 million, Bioverativ: €108 million, Boehringer Ingelheim CHC business: €56 million, Aventis: €44 million) and to acquired intangible assets (licenses/products: €22 million) was recorded in the fourth quarter. These items have no cash impact on the Company.

- An impairment of intangible assets of €3,604 million mainly related to Eloctate® (€2,803 million due to revision of sales projections), Zantac® (€352 million), sotagliflozin and Lemtrada®. The fourth quarter included an impairment of intangible assets of €1,581 million of which €1,194 million related to Eloctate® and €169 million to Zantac®.

- Restructuring costs and similar items of €1,062 million (of which €158 million in the fourth quarter) mainly related to streamlining initiatives in Japan, Europe and the U.S.

- An income of €238 million mainly reflecting a decrease of Bayer contingent considerations linked to Lemtrada® (an income of €214 million of which €74 million in the fourth quarter), a contingent price adjustment on the disposal of SP MSD (€192 million) and a fair value remeasurement on the CVR price (a charge of €49 million of which €32 million in the fourth quarter).

- A net income of €327 million (of which a charge of €67 million in the fourth quarter) mainly related to litigation.

- A €1,866 million tax effect arising from the items listed above, mainly comprising €1,409 million of deferred taxes generated by amortization and impairments of intangible assets and €311 million associated with restructuring costs and similar items. The fourth quarter tax effect was €587 million, including €503 million of deferred taxes generated by amortization and impairments of intangible assets and €64 million associated with restructuring costs and similar items (see Appendix 4).

(9) See Appendix 3 for 2019 Fourth-quarter consolidated income statement; see Appendix 11 for definitions of financial indicators, and Appendix 4 for reconciliation of IFRS net income reported to business net income.

- An expense of €165 million net of tax (of which €71 million In the fourth quarter) related to restructuring costs of associates and joint ventures and expenses arising from the impact of acquisitions on associates and joint ventures.

Capital Allocation

In 2019, Free Cash Flow (see definition on Appendix 11) increased 48.6% to €6,026 million, after net changes in working capital (-€580 million), capital expenditures (-€1,405 million) and other asset acquisitions1 (-€576 million) net of disposal proceeds1 (€490 million), and payments related to restructuring and similar items (-€1,142 million). Over the period, the dividend paid by Sanofi was €3,834 million and proceeds from disposals2 were €672 million. As a consequence, net debt decreased from €17,628 million at December 31, 2018, to €15,107 million at December 31, 2019 (amount net of €9,427 million cash and cash equivalents).

1Not exceeding €500 million per transaction.

2Amount of the transaction above €500 million per transaction.

To access the full press release of the 2019 Q4 and full-year results, please click here.

Financial statements are not audited. The audit procedures by the Statutory Auditors are underway.

Forward-Looking Statements

This press release contains forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995, as amended. Forward-looking statements are statements that are not historical facts. These statements include projections and estimates and their underlying assumptions, statements regarding plans, objectives, intentions and expectations with respect to future financial results, events, operations, services, product development and potential, and statements regarding future performance. Forward-looking statements are generally identified by the words “expects”, “anticipates”, “believes”, “intends”, “estimates”, “plans” and similar expressions. Although Sanofi’s management believes that the expectations reflected in such forward-looking statements are reasonable, investors are cautioned that forward-looking information and statements are subject to various risks and uncertainties, many of which are difficult to predict and generally beyond the control of Sanofi, that could cause actual results and developments to differ materially from those expressed in, or implied or projected by, the forward-looking information and statements. These risks and uncertainties include among other things, the uncertainties inherent in research and development, future clinical data and analysis, including post marketing, decisions by regulatory authorities, such as the FDA or the EMA, regarding whether and when to approve any drug, device or biological application that may be filed for any such product candidates as well as their decisions regarding labelling and other matters that could affect the availability or commercial potential of such product candidates, the absence of guarantee that the product candidates if approved will be commercially successful, the future approval and commercial success of therapeutic alternatives, Sanofi’s ability to benefit from external growth opportunities, to complete related transactions and/or obtain regulatory clearances, risks associated with intellectual property and any related pending or future litigation and the ultimate outcome of such litigation, trends in exchange rates and prevailing interest rates, volatile economic conditions, the impact of cost containment initiatives and subsequent changes thereto, the average number of shares outstanding as well as those discussed or identified in the public filings with the SEC and the AMF made by Sanofi, including those listed under “Risk Factors” and “Cautionary Statement Regarding Forward-Looking Statements” in Sanofi’s annual report on Form 20-F for the year ended December 31, 2018. Other than as required by applicable law, Sanofi does not undertake any obligation to update or revise any forward-looking information or statements.